This Week To Watch:

Monday, April 21, 2025

The Amazon Dynamic:

The Amazon Dynamic:

Air Service at Small Community Airports & Defunct Shopping Malls

Speed of communication.

Write this down. This is the #1 factor that drives demand and value for just about everything in commerce and general living.

Let’s take retailing. Fifteen years ago, the most time-effective way of buying stuff was to hop in the car and go to the nearby shopping mall. Today, YouTube is rife with coverage of dead and dying malls across the USA.

The point: people are still buying things, but there are increasingly better and more time-efficient channels that have supplanted brick and mortar shopping.

Some Small Community Airports Are Like Dying Shopping Centers. Speed of communication. It’s what a number of small communities that are seeking air service miss: the main advantage of local flights has been leapfrogged by other air service options.

The consumer has other better options, just like the folks who aren’t heading out to the mall, anymore.

In determining the value of local air service options, the dynamic of competitive speed is usually ignored in most pandering ASD studies done for small community airports.

Historically, the fastest major channel of moving important data and physical interaction was by air. Transporting the important document or personnel expertise as fast as possible meant flying to New York or wherever, meeting with other humans and flying back.

Today, the info is already electronically disseminated from the gitgo. The need to belly-up with colleagues in many cases is no longer needed, and in others it’s done by video.

Point: the efficiency of air travel as a communication modality is now far less for some applications than it was as recently as five years ago. Like shopping, communication continues, but through different modalities.

So, like the defunct shopping malls, a lot of formerly viable air travel applications are no longer needed.

Cutting to the chase. Just saw where Pueblo, Colorado will be getting roughly two EAS flights on Denver Air Connection to Denver. Cheers throughout the community, looking for reliable air service.

It won’t carry diddly, regardless, because it is completely inadequate in delivering air transportation that is superior in travel time (speed) to other options. Like, a 40 minute or less drive to COS to access 38 departures a day, on five airlines to seven true connecting hubs. Certainly, DAC is a fine operator, but those EAS flights cannot compete.

With just two departures to shoehorn a journey into, what taxpayers are shelling out for EAS at Pueblo is a DOGE-level national scandal. The myopic and parochial nonsense about the importance of service at the “local airport” is nothing the city should be proud of.

What is very strange is that all of local media in Pueblo are comparing the DAC service only to the longer drive to Denver. As far as they are concerned COS may as well be chopped liver, when in actuality and in geographic location and in levels of service, Colorado Springs Airport is the actual gateway for Pueblo and south on I-25.

Naturally, there probably have been the perfunctory “catchment studies” that prove that there are gazillions of people in the region that airlines will be thrilled to hear about. And maybe the local surveys that include nothing more than where local folks would like to fly to, with not any info on fares or schedules.

Snake oil. Just one honest analysis of regional access and the realities of the air transportation system would avoid these scams.

This is not to single out Pueblo. It is just a poster child for the airport-to-shopping-mall dynamic. Just saw where Ft. Pierce in Florida and a small community in Mississippi have apparently been convinced that “air service” is coming. It’s bordering on a national scandal.

Nuff said. The #1 dodge in ASD programs today is intentionally not bothering to see what the alternative communication and air access channels the local airport must compete with. It’s all about trying to fantasize that consumers will act irrationally just to use the local airport. It’s founded on the fantasy that a flight or two at the local airport is “air service” sort of like plugging into an electrical socket.

Air service planning in the future must be part of “regional economic planning” instead of chasing air service that’s inferior to consumer alternatives.

It is inevitable, but in the meantime lots of money will be spent on chasing ASD skyhooks in lieu of hard economic development programs.

__________

This Week To Watch:

Monday, April 7, 2025

Advantage: DL/UA

The ULCC Invasions of Majors’ Hubsites:

Success Will Be Determined By Customer Service.

The battle is joined.

We’ve covered this over the past year. ULCCs (with the “U” removed, actually) trying to break unto core major airline hub markets.

We see Frontier adding flights big time at Delta’s Atlanta hubsite. Spirit doing the same at Detroit v Delta. There are variations, such as Frontier expanding at SAN and Spirit at SAT. Less direct head-to-head compared to attacking connecting hubs where the major has the advantage of flow traffic. But the outcome will still be determined by one foundational factor:

Customer service. The Product.

The way passengers are treated and dealt with from the time they book until they get to the airport curbside at the destination. As we’ll see, this is not a matter of just low fares. In fact, there’s some indication that at the end of the computation, the former (U)LCC may not have much or any real advantage in what the customer pays.

There is an open but unrecognized question whether these airlines have the structure and the IT to compete with United and Delta. This is a different air service system from just a couple of years ago. Historically, airlines sold a ticket, and the passenger traveled. Problems on the journey were handled after they occured, and not really well, either.

Today, carriers like United are selling a product that includes systems that anticipate effects of IROPs and proactively address them with the customer. (U)LCCs are at a disadvantage – generally they don’t have the structures to compete with these services. They may be bringing a Ginsu knife to a gunfight.

Example: Frontier/Atlanta – A Cursory Look.

One heavy assault – among several – is Frontier’s expansion at Atlanta. This would be a preview for Spirit’s just-announced major expansion into Delta’s Detroit hubsite.

Lots of Unknowns. The open questions are many. Can the total of low fares plus ancillaries attract local O&D traffic from Delta? Or, attract net new demand? What about brand-identity? How ’bout minimal day-of-week scheduling in competition with high frequency Delta service subsidized by flow traffic?

Lots of Unknowns. The open questions are many. Can the total of low fares plus ancillaries attract local O&D traffic from Delta? Or, attract net new demand? What about brand-identity? How ’bout minimal day-of-week scheduling in competition with high frequency Delta service subsidized by flow traffic?

Delta Sky Miles program loyalty is a question. Another is the levels of customer service contact. United, for example, is clearly gunning for ULCCs (and everybody else) by leveraging its massive IT investment into customer contact and support.

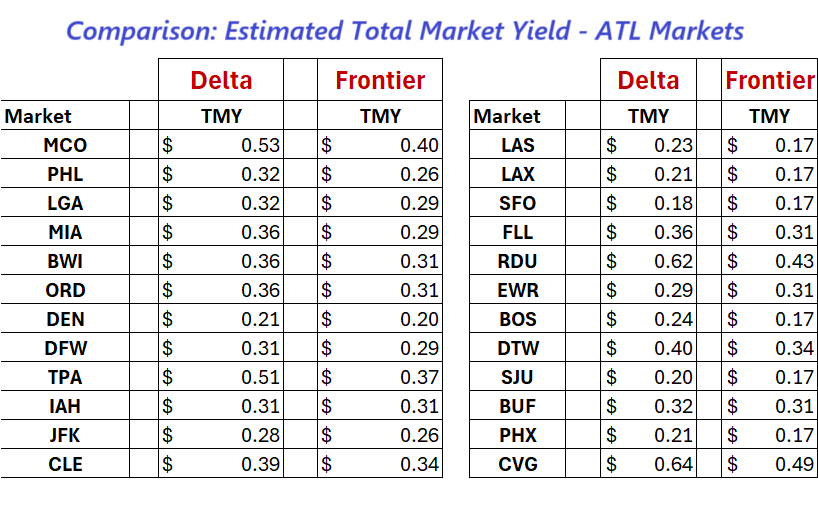

The (U)LCC Might Not Have A Consumer Cost Advantage. Using numbers from our friends at Airline Data for the 4Q of 2024, we took a shot at what the real passenger cost variances might be between Delta and Frontier.

As any professional analyst understands, the “fares” as reported in DOT tables are derived from the fare on the ticket. But today, particularly at ULCCs, it is the added ancillary fees paid by the passenger that actually represent what he/she is charged.

We looked at the “fare” for each of 23 competing markets, and factored in reported additional bottom-line ancillary percentages. It’s reported that the ticket fare at F9 is only about 35% – 40% of what passengers cough up to fly Frontier.

Because Delta is not ancillary-focused, and there is confusion about just what is an “ancillary” (excess baggage? legroom upgrades? – the determination varies in the DOT reports airline to airline) we estimated that Delta’s reported fare yields are closer to 90% of total passenger billing.

These rough numbers – and, friends and neighbors, they are very first-pass bumpy – it would appear that by the time the customer buckles the seat belt, the actual cost between Frontier and Delta might not be all that substantial.

Skewing these data are the differences in the passenger bases at each carrier. Frontier is basically one product, give or take a couple of “Big Seats” and a legroom segment. The Delta numbers are inclusive of business class and premium economy passengers, which inflate the average per-mile raw fare yields. That would indicate the the consumer-paid yields in the Delta economy cabin are likely lower than shown here.

Bottom line: at the end of the journey, Frontier might not be that much cheaper to fly than Delta.

Nevertheless, in most of these markets in the 4Q, Frontier was hitting load factors at or above 85%.

This could be due to the initial fare attracting passengers, or it could be due in part or all to the fact that Delta also had load factors at ATL that could make the F9 entry a lot easier.

Now, that much said, the issue is whether Frontier can gain a solid consumer identity in the Atlanta market.

Customer Service Delivery: The Deciding Consumer Success Factor. Looking at the initial data, it would appear that much of the Frontier success (we assume that’s what the bottom line would show) is due to capacity/demand factors, and not due to any cost advantage to the consumer.

In fact, there are some new clouds on the horizon in this competition. Delta has implemented sophisticated IT programs that have materially made turn times at ATL far more efficient. They have the infrastructure and schedule frequencies to rapidly accommodate and remediate IROPs and their effects on their passengers.

In the absence of anything but an apparent first-pass, pre-ancillary fare differential, Frontier has a very real challenge. They need to be able to provide a customer service product that can compete with what Delta (and United, for that matter) can and are delivering to the customer.

And that is the bottom line: Frontier and Spirit, if they are to succeed in this type of expansion, must turn every passenger into a future customer. There are lots and lots of people that will first-time-try a new airline. If they don’t come back, that’s another issue.

It appears that Spirit understands this, at least in initial phases.

Frontier may be on a different philosophy. It’s not an indication of service orientation when a senior executive, referring to passengers who try to skirt certain fees as “shop lifters” or petty thieves. (May be accurate, but pretty untoward to launch this out in public. Deal with it quietly instead of appearing tell the world that you consider some of the passengers you carry to be street scum.)

Then, it is the nadir of service orientation to pay contract gate staff a “bounty” to cruise through the gate lounge to seek out and “apprehend” passengers with carry-on that is even a centimeter bigger than the sizer and then deny them boarding unless they pay a sudden $99. Not cool. Matter of fact, the kangaroo congressional airline hearings a few months ago got high-centered on this, implying that this type of shenanigan was typical across the airline industry.

Actually, this concept of customer service was summed up well in the latest industry analysis by Swelbar-Zhong:

“… And while we are at it, Frontier announced they would stop using jet bridges as a way to save money and speed its boarding process. Is it now part of the premium bundle to walk in the rain to find the big chair?”

Again, the future is in providing service that entices the passenger to prefer the airline.

United understands this. Delta understands this. The historical service at Southwest understands this. It’s apparent that newcomers Avelo and Breeze understand this.

More and more, the consumer will demand this. Success will depend on it.

__________

March 31, 2025

Emergence of New Airline Category:

National Carriers

Anybody notice what Frontier and Spirit and to a lesser extent both Avelo and Breeze are doing?

They are implementing a new air transportation sector. I would call it the “national” carrier system. Add capacity in key markets dominated by a major airline, and see if the consumer will use it.

The general strategy is to be a secondary player in high-density markets and become an additional consumer option at airports where one of the four majors (AA, DL, UA, WN) have set up connecting hub operations.

The presence of these carriers isn’t exactly turf-based, but it is focused on operating at the margins of the dominant carrier’s route system. It’s piggy-backing on major airline capacity where there could be sufficient consumers to make it work. Three flights a week where the major has three a day.

Take a look: CLT, DFW, DTW are examples where this strategy is being tried.

Traditional thinking is that it won’t work. But this isn’t tradition. And the folks running these airlines didn’t just fall off a turnip truck, either.

This is now a world where brand loyalty isn’t driven as much by frequent flyer programs, particularly for non-business customers.

Stand by. This could change air transportation. Or, it could fizzle.

We’re watching.

_________

Airline Industry Rite Of Passage

As of this Friday, Air Wisconsin will no longer be leasing lift to the American Airlines system. That leaves what looks like 60 CRJ-200s out of the scheduled skies. The carrier has indicated it will pursue charters and EAS flying.

Watch for the usual suspects to decry this as one more outrage inflicted on small airports. The real message is that air service won’t miss beat. AA is just replacing an operator, not dropping markets. In fact, it appears that the CRJs are being replaced with E175s, which comfort and cabin-wise is a mainline travel experience.

________________

Air Traffic Control:

Going Nowhere, But With Delays Enroute

Have received some feedback already from this week’s Touch & Go™ which took a somewhat iconoclastic view of DOT secretary Sean Duffy’s ATC announcement at a Cabinet meeting.

Cut Him Some Slack. The feelings are that the guy is new, and he’s been kicking tush and taking names in the short time he’s been in the job.

Yup, that is true, and Mr. Duffy is a whole lot more of substance than the political mannequin he’s replacing. He’s in a different galaxy from any of his predecessors. LaHood? Chow? Cadavers would have delivered better leadership.

But everything Mr. Duffy said about fixing ATC has been said before. And nothing has been done. He’s looking at the symptoms that have traditionally resulted in past ATC programs.

The reason is that the approach is to build an ATC system and then have the user base accommodate it.

This time around, the DOT must start by defining the performance metrics the system must deliver. Not throw-away platitudes like “safety” or “efficiency” – but instead hard standards and systems to achieve these goals consistent with demand.

Standby For Disruptive Concepts. In the next Touch & Go™ we’re going to outline what the new ATC system should be developed to deliver. Captain Michael Baiada has a number of points that need to be discussed before anybody at DOT starts ordering flash drives to replace floppy disks. And, yes, the airline industry needs to change its MO, too. They and their passengers are being shafted by the FAA’s inept work. Stop “partnering” and stop tolerating the agency’s inept work.

If you’re not on the T & G list, drop us an email and join the over 500 aviation leaders who get it every Saturday.

__________

Monday, March 24, 2025

Observations For This Week

Item: Major Security Failure At London Heathrow

Here’s a flash: what happened last week at Heathrow when the entire airport got shut down was in fact a major security failure.

The media simply reported it as just a gigantic electrical outage. The reality is that Heathrow has a very glaring security problem.

Earth to the airport industry: This is a wake-up call.

When an airport is brought down, by whatever means, it is an event that affects the viability of the facility. It doesn’t need to be blown to smithereens. The hard truth is that Heathrow was completely shutdown, imposing massive financial damage to all concerned.

Security is the protection of assets from untoward events. It’s a whole lot more than just intercepting some clown with a pocket full of C4. Security means making sure that what happened at Heathrow is taken as a failure to protect the airport and the public.

Harsh but true – this is one more example of how “security” is considered to be just stopping guns and knives and oversize bottles of Grecian Formula from getting on airliners.

It is a lot more than that. It means having programs in place to anticipate and deal with potential security threats.

How many airports in America have fully-vetted event contingency plans? How many airports in America have event mitigation and event remediation plans? How many airports have security programs for the systems that support the facility, like HVAC?

It’s pretty clear that Heathrow didn’t.

Security planning is anticipating events that can threaten the viability and safety of our assets.

And that includes the propensity of blowing a fuse at the wrong time.

____________________

Item: Southwest Transformation. Is The Customer Involved?

The continuing news out of Southwest is not particularly encouraging.

It is becoming very obvious that Elliott Management has the brilliant idea that if they make WN look just like every other airline and adhere to their template of what an airline should be, shareholders will be just thrilled with the increase in the stock price.

Take a gander at the news coverage of what is supposedly being planned for the Southwest product. The fear is these are being accomplished simply to give shareholders the impression that WN is now going to be just like every other airline.

Missing from all of this is any discussion of how the proposed changes enhance the customer experience. Or how it will get more passengers to want to fly Southwest.

It’s very clear that these changes are all about bringing in more fee and fare revenue – and not more customers. Every one of these initiatives is focused on how to get more long green from existing passengers.

Two weeks ago on LinkedIn I outlined briefly how these changes somewhat mirror the dim bulb changes that were made at Braniff International in its last six months. Dimbulb changes that did not involve making the product better for the customer sent the airline directly into the ground.

The over 50 thousand impressions and positive comments about that post would indicate that a lot of folks out there also see it this way.

___________________________

Item: Adios, Air Wisconsin. Lots of Futurist Messages

As of April 4, Air Wisconsin will be replaced as a contractor at American Airlines.

Air Wis has painted this to look somewhat like it was their decision and they’re going to be moving on to doing charters and essential air service flying.

We wish them the best, but placing about 47 CRJ-200s that are now operating at American Airlines is going to be pretty tough.

What is of interest is that this includes grounding of over 500 pilots. It comes after pilot cutbacks at FedEx and cutbacks at Spirit and hiring freezes at Southwest.

Yes, there is a pilot shortage but it’s not manifesting in pure mathematical results.

Another message here is that the majority of “regional airlines” – or more correctly small lift providers – are now owned and or controlled by major carriers. The days of turf-focused independent regional airlines died a quarter century ago.

This, plus the materially increased operational costs of smaller jets, has raised the bar for air service recruitment at many smaller communities. And that won’t change.

Lots of messages here regarding the evolution of air transportation.

___________

Item: FAA Administrator Nominee.

The aviation industry should be flat out thrilled with the nomination of Brian Bedford to be FAA administrator. He has the qualifications and the expertise in the background to address the administrative and strategic rot that has engulfed the place.

As I pointed out on this week’s Touch & Go™ vision letter, we can expect some of the usual suspects to come out of the woodwork to throw rocks at Mr. Bedford. One supposed prestigious travel magazine – Fodor’s – posted a dishonest headline stating that this man has actively reduced aviation security over the years. It’s a lie but it’s a politically correct lie in a number of circles.

It’s time that aviation leaders come out and support Mr. Bedford, as I suspect we will have several vested interests instructing their wind-up toys in Congress to attack him viciously in the confirmation hearings.

If you’re not on our TNG distribution list, you can click here to take a look at what was posted. And if you aren’t on the list, drop us an email to join the over 500 aviation leaders who receive it every weekend.

_____________________

Monday, March 10, 2025

Elliott & Southwest:

We’ve Seen All This Before.

And It’s Not Real Comforting.

In any business, the product/service model and the market strategy are the foundation of success or failure.

The fact is that this strategy needs to constantly be modified to accommodate anticipated changes in the market.

A Look At Wreckage Is Splattered Across Several Industries. Anybody remember Sears Roebuck? Into the 1970s it was America’s largest retailer. Today it’s down to less than a dozen stores across the nation. Reason: changes took place that rendered Sears to have no competitive advantages in retailing.

A Look At Wreckage Is Splattered Across Several Industries. Anybody remember Sears Roebuck? Into the 1970s it was America’s largest retailer. Today it’s down to less than a dozen stores across the nation. Reason: changes took place that rendered Sears to have no competitive advantages in retailing.

The Beer That Made Milwaukee Famous. At one time Schlitz was America’s largest selling beer. Cutting to the chase they messed around with cheapening their brewing process to the point where the customer didn’t recognize it anymore. The objective was to enhance shareholder value. And it certainly did for brands such as Budweiser.

Let’s talk about some airline examples.

Midwest Airlines was once incredibly successful, because like WN, it had a product that was differentiated from other airlines. A high cost one, but initially brand loyalty made it happen. A business class product featuring complimentary wine, incredible food and airplane cabins that smelled like fresh baked cookies. But with changes in economics after 9-11, Midwest financially couldn’t maintain that product, couldn’t find another one, and is now gone. The product went away.

Then there was Braniff International. This one is directly instructive for Elliott management. There is lots of silly lore about the first major airline to go “chapter,” but the hard truth is that Braniff underwent an experience not too different from what may be going on today at Southwest.

Here’s the lesson in airline 101: Messing around with the consumer product and consumer loyalty in order to “enhance shareholder value” can be lethal. When the customer no longer recognizes an airline, customer loyalty goes away, and that’s not good for the bottom line, usually.

In 1978, Braniff had the strongest margins and among the lowest ASM costs in the business, along with a reputation of industry-leading inflight service and innovation. Leather seats. Middle seat fold-down in coach. Cappuccino. First class with caviar and entrees cart-served at the passenger’s seat. Designer employee uniforms. A flexible and aggressive management that could take advantage of opportunities fast and effectively. Strong brand loyalty.

Then came deregulation. Braniff opened 14 new domestic stations on the first day, then went on to shoot new orange 747s across the Atlantic and the Pacific. But a sudden and unanticipated spike in fuel costs, and 20% interest on the financing of dozens of new airliners, by the end of 1979 generated tank trucks of red ink.

In mid-1980, changes took place. The formerly-worshipped CEO was canned, and a gentleman named John Casey was moved up the ranks. He successfully renegotiated debt payments and achieved cooperative labor concessions from Braniff’s unions. Cut out virtually all of the long-haul flying.

By mid-1981, Braniff International was reporting operating profits. Not all-up, due to high debt, but it was making money again flying passengers. Then, the board of directors got antsy, and decided to bring in a true messiah team to run the airline.

And run it they did. Right to the point of financial impact, all the while touting how the airline was being transformed for the future.

You guessed it. The goal was essentially “to increase shareholder value,” completely oblivious to the airline’s customer base. (Elliott: you getting this picture?)

Braniff’s single and historical market advantage – a superior inflight product – was gutted without any concern for the consequences. It’s ironic that the new messiahs were intent on taking the structure and systems of a full-service airline and trying to remake it into a clone of Southwest. Nice, but nobody considered that the customer base and revenue foundations of the two airlines were very different.

Out with first class, driving off a huge chunk of formerly loyal business travelers. Ditch most of the inflight amenities. Cram more seats on the 727s. Schedule more flying, even when traffic might not be there, to look good spreading more ASMs over existing fixed costs, even if the seats were empty. Implement a “simple” two-tier low fare structure to look like a bargain airline. A system that competitor American easily matched, even as they welcomed Braniff’s former business customers onto their airplanes.

It took a little more than six months before all this transformative magic rendered Braniff unable to make payroll.

History message to Elliott: what the new team did was completely change the factors that supported the airline’s brand loyalty. The consumers really had no reason to fly Braniff compared to the competition.

There’s a message here, flower children at Elliott.

In any business, it’s the product that brings in the dough, and if the product isn’t one the customer recognizes as better, things go 86 fast.

That may be happening at Southwest.

Think about it, flower children.

________

Monday, March 10, 2025

RIP: Russian & Chinese Airliner Programs

If there was any chance of Russian and Chinese airliners getting into the global market, it’s really dead now. Fuggetaboutit.

There have been some silly news articles illuminating the shortfalls of Boeing production and the full order book at Airbus and concluding that this is an opportunity for Russian and Chinese airliners under development.

A return of the Douglas DC3 has a better chance of breaking into the market than any of the lead sleds that are being produced in Russia. Or in China.

Between the Ukraine war and the brutish behavior of the thugs putting China’s economy under, no sensible airline outside of the native countries would place an order for these lead sleds.

The Russian MC-21 and SJ-100 programs look great to the uninformed. But neither has anything to offer that represents an advantage over current programs at Boeing, Airbus and Embraer. As a matter of fact, they are vastly inferior.

But now, with the embargo on Russia due to the Ukraine war, both of these airliner programs are being forced to be re-designed with Russian engines, Russian avionics, and Russian subsystems. None of which are proven and none of which have any chance of developing a global support system.

Say good-bye.

‘Course, we have the clowns running China trying to push the C-919, the C-909 and the still-on-paper C-929. The problem there is that not only are the first two bow-wows in performance but – unreported – they too could get zapped by a pulldown of western technology.

Kid yourself not, at Zhongnanhai – sort of the local version of the White House in Beijing where the CCP thugs confer – things are not all jasmine tea and hibiscus flowers. The country is in trouble economically and diplomatically. Remember that the USA suppliers to Chinese airliner programs are there mostly to assure a piece of the action.

But if it continues to become obvious that these airline programs are going nowhere, i.e., there will be no “action,” the enthusiasm at USA suppliers will evaporate. If the aircraft aren’t going to sell, then suppliers won’t be all that excited about sucking up to them.

Further, should there be any military action against Taiwan (and, if so, it will be quick lightning and a lot less dramatic than a replay of The Longest Day) then all USA support for any CCP aviation programs goes 86.

Point: Even with Boeing’s problems, the full orderbook at Airbus, and Embraer seeing a scope-driven market brick wall for the E175-E2, these are the only three places where airliners will be coming from in the future.

As they say at the pool hall, this runs the table in regard to airliner production.

___________________________

Monday, February 24, 2025

Silver Airways:

Witnessing The Swan Song

of The Regional Airline Industry

It was just reported that Silver Airways suddenly cancelled their entire schedule at Orlando. No warning.

Still flying elsewhere, as far as is known. What is pretty much the future picture is that the MCO announcement is part of a trend.

This is not just another route announcement. With Silver, we are witnessing the swan song of a specific air transportation modality that long ago became obsolete.

It’s called independent regional airlines. These were the carriers that had their own market turf, sold their own tickets, collected their own revenues, had their own fleets of turboprops (mostly), and operated under their own market identities. Silver is one of the very few left. Actually, maybe the only one left of that genre.

Silver filed Chapter 11 last December, with the usual eager pronouncements about reorganizing into a stronger airline, etc. However, the reports of unpaid airport rents and charges and concerns about the deposition of PFCs collected from passengers that are required to be transmitted to airports brings some reality into the picture.

It’s The Marketplace, Not The Airline. Let’s cut to the chase here. This probably isn’t a case of a company intentionally trying to defraud airports and the public. It’s likely not even the outcome of mismanagement. It’s much simpler: the entire market foundation for independent intra-regional airlines is gone. Evaporated. Dried up. Silver has been trying to fill a need that no longer exists in the volumes that can support the costs.

The reason is the evolution of communication channels. Intra-regional commuter/regional airlines once had a role. Today, the combination of electronic communications and raw cost economics are such that the “regional airline industry” has atrophied. It is obsolete to the needs of the economy.

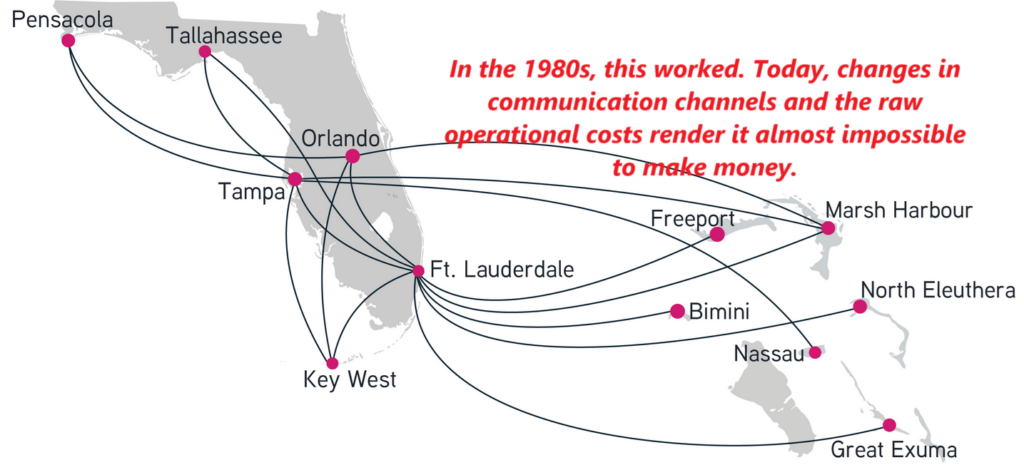

Forty years ago, when carriers of this genre – operating their own geographic route system reselling their own tickets, taking their own reservations, etc. – were in full operation, there was a need for getting people and the information they possessed from BDL to NYC, or ABI to AUS, or BOS-ISP – and dozens of dozens of others.

The main emerging shortfall of traditional independent, turf-dependent regional airlines is the issue of time. In the types of markets noted above, they were successful because it transported information and data, in the possession of human mules (a bit indelicate, but accurate.)

Now, the time necessary to get to an airport, board a flight between BGR and BOS, go to the meeting, and come back is incredibly onerous, inefficient and expensive.

Now, the time necessary to get to an airport, board a flight between BGR and BOS, go to the meeting, and come back is incredibly onerous, inefficient and expensive.

So, what needs to be tumbled to is the hard truth that there is a whole new – and continuing to evolve – set of communication systems in a modern economy.

Fleets of independently-operated O&D ATRs or even long-gone Metros and 1900s, simply cannot compete any longer. Add to this that the raw costs of operation of machines – even like top-shelf ATRs – have priced out a lot of leisure as well as business demand.

RAA: Call A Good Corporate Identity Consultant. It’s another reason that the Regional Airline Association really needs to search for a new name. The “regional airline” system they once represented is gone.

______________

Monday, February 24, 2025

The New DOT Secretary:

We’ve Found A Winner For All Transportation Modes.

Sean Duffy barely had time to order a Starbuck low-fat latte after his swearing in before a phalanx of aviation events came over the transom.

Sean Duffy barely had time to order a Starbuck low-fat latte after his swearing in before a phalanx of aviation events came over the transom.

The Potomac tragedy. The medevac crash in Philadelphia. The Delta event in Toronto. Plus, bush operation crash in Alaska and GA midair in Arizona which got press in the shadow of the larger events.

And Mr. Duffy was on top of it all. No jive. Just hard information and attention. Remember, aviation is just one area of his new remit. There are roads and bridges and all manner of other transportation channels he is responsible for.

The main observation is that it appears that trendy political correctness is not his strong suit. Along with the aviation matters, Mr. Duffy has literally grabbed a third rail: he’s asking hard questions about the loony SFO-LAX high speed train project in California.

‘Course, any semi-literate grade school kid could see how this bazillion-dollar golden idol of dimbulb progressive thinking is based on complete lies. The lie is in the implication that it will actually connect the downtowns of both cities. Or the lie that it will be high-speed transportation, when every political fiefdom it would travel through will demand a stop. (Any guess on how long it takes a train to get up to 125 MPH, and how long it takes to get it to stop? Rapid transit it is not.)

Then there is the nonsense that it will compete directly with air travel and in the process take nasty CO2 out of the air. No telling what the environmental hits will be in building this contraption.

Governor Newsome isn’t happy that one of his pet projects is being questioned. The luddite passenger rail groupies aren’t popping the bubbly, either.

But with what we’ve seen in the last three weeks, maybe the USA traveling public might want to raise a glass.

____________

And As One Example Of The New Tenor In DOT:

Buttigieg’s Parting Shot Says It All

Compare and contrast what we’ve seen with Sean Duffy and the four years of slick dance moves by his predecessor.

The occasional press conferences laced with semi-accurate information were just the start. But in his last month, Buttigieg did the airline industry a favor in one action that defined not only himself, but once again proved that as far as finding truth and facts, some parts of the aviation media are more like a cesspool than a flow of accurate information.

In a grand splatter, Buttigieg announced substantial punitive fines on Southwest Airlines for multiple 3-plus hour “tarmac delays.” This was duly trumpeted in most of the media and on the Walter Mitty hobbyist aviation websites that posture themselves as experts. Shame on Southwest!

The only problem was that Buttigieg’s hoodlum staff dug up “delays” that had occurred more than two years earlier. Like, how many schedule changes and operational shifts has WN taken since then? Without question, this was cheap political grandstanding that had no effect on improving anything except Buttigieg’s expertise as a cheap political seat warmer.

The other lesson is that we are pretty much on our own when it comes to ferreting out honest aviation information. There was nary a single media outlet that illuminated the dishonesty of the stunt.

That also means that a lot of the veneer aviation Fourth Estate will have Mr. Duffy in the cross-hairs.

__________

__________

Monday, February 17, 2025

FAA: Air Traffic Control Is Not The Problem.

It’s Just One Symptom.

Get ready. This week, the air traffic control system will be front and center.

It’s been reported that the administration’s DOGE team will visit the FAA ATC command center, and later visit the ATC training facilities in Oklahoma as well.

The usual battlelines are drawn.

The DOGE people are looking to zap waste and mismanagement. On the defense are the literal herd of oxen in line to get gored and their political operatives who are in full metal jacket mode to protect the waste supporting their jobs.

Politicians who just months ago eagerly supported a nominee for FAA administrator who had essentially zero understanding and background for the position, and literally had no fundamental suggestions, are now righteously stating how people like DOGE with no experience should be denied entry to the building.

Hypocrisy is in full bloom.

And everybody is on the narrative that it’s all about more funding, more training, and more people at ATC centers. That’s the solution.

No. That is the problem. It’s been implemented as the solution for decades.

Let’s dump a downpour on this trendy narrative parade.

As is stands today – just about all sides in this babbling political street fight are not only wrong, but are themselves a major part of the reason the FAA and ATC is a festering outrage.

All of them. That’s because as of this moment the “solutions” are aimed at “fixing” the FAA as is, where is, and pretty much in place.

New Paint For A Rotted Structure. Except for folks just arriving back from an extended vacation on Pluto, it’s a dodge to ignore that the FAA needs to be gutted, re-focused and rebuilt. Not repaired. Rebuilt from the inside out.

What’s going on today is packs of politicians – themselves who couldn’t tell the difference between a Cessna 172 and a Mounds Bar – are locked in a battle to retain and protect the bureaucratic morass that the FAA has been mismanaged into. That’s all sides, at least as it appears today. DOGE finding waste at the FAA is like discovering garbage in a waste site.

Get this. It is the entire Federal Aviation Administration that’s the problem. Front door to the fire exit. The air traffic control system is just one part. It’s the part that affects the public the most, but there’s a lot of inefficiency, financial rot and incompetent management in other departments down the hall from the ATC folks.

The Federal Aviation Administration is just that – and aviation-related entity. Ever taken a gander of the bazillions of FARs that regulate aviation?

That includes things like airport oversight and regulation. Things like regulation and oversight of aviation suppliers and OEMs. Approval and monitoring of grants and discretionary funds. Literally hundreds of oversight and regulatory responsibilities.

Point: from the experience at hand over the last three years, there should be a lot of questions and investigation of a lot more things at the bottom of the FAA bird cage than just ATC.

How about oversight of Boeing? Regardless of the drivel put out by the last and now-skedaddled administrator, it was the FAA’s responsibility to provide independent oversight over things like the 737Max program. They incompetently failed. Two crashes occurred that have been connected to questionable oversight and implementation.

Then how about the professional FAA corrosion uncovered with the Alaska Airline 737 plug failure, which came an ace and a couple thousand feet of altitude from a major crash. Seems there were no records of the technicians who had improperly done the repair. They are apparently still on the loose in the Boeing facility. In the airline industry, these records are required and essential. Not so, apparently, when Boeing was turning the wrenches. The FAA didn’t care.

Worse, this was during the post-Max “heightened” FAA oversight of Boeing. Needless to say, nobody has been fired at the FAA, and they have simply skated along, basking in the sunshine media reports based on the PR babble put out from the FAA itself.

‘Nuff said.

Let’s watch what comes out of the DOGE investigation.

Message to Elon: It’s a whole lot more serious and more fundamental than over-staffing, poor record-keeping and some senior posts being staffed with mannequins nominated by dishonest Senators.

It is about safety and the future of America’s aviation industry. DOGE needs to discover more than financial waste at the FAA.

They must be the start of rebuilding the entire agency.

______

Frontier Acquisition of Sprit:

The Main Result: More Uncertainty

Before We Start: Quote of The Week:

“Now is not the time to put someone with zero experience in dealing with our national air traffic controllers into any position of authority.”

Rep Tim Kennedy, D-NY, in regard to DOGE investigating the reasons and solutions for the national shortage of air traffic controllers.

Funny, but a news search done high and low reveals nothing from this august solon denouncing the nomination of Phil Washington – also with zero such experience – to be FAA administrator.

He might have missed it.

___________

Regarding Frontier Offer For Spirit –

Outcome: Merging Lots of Uncertainty

In any product market, one immediate turn off for the consumer is uncertainty.

Uncertainty regarding the identity of the product. Uncertainty regarding the competitive quality of the product. Uncertainty regarding the market stability of the product. Uncertainty regarding the service delivery and value of the product.

Uncertainty represents risk. When consumers have an alternative, they avoid risk.

That seems to be what’s affecting the efforts by Frontier and Spirit to break out of the collapsing ULCC model by attempting to expand into core business markets.

Now that the “U” is gone, and the “L” is a lot less at variance with major carriers (figure it out for yourself), a low fare alone is not as compelling – nor as possible – as it once was in getting consumers to book on an airline they really don’t know much about. Particularly one that might only offer a couple flights a week to a given non-leisure destination.

Frontier has made a move to acquire Spirit. The combined entity would entail a total fleet of approximately 328 A320/321 airliners. Plus – at least on paper for now – another roughly 280 more on order. Lots of flying machines.

It is entirely accurate that putting both carriers together as a merged operation would likely slash overhead costs of the combined entity by a significant number.

The usual veneer media suspects are publishing dot maps showing airports where the two airlines operate, with throw-away lines like “it’ll be the fifth largest airline!” What they leave out is the market dominance – or more accurately, the lack of market awareness – of these carriers in each of the map dots. That’s uncertain.

Take a look at the many non-leisure markets both Frontier and Sprit have jumped into and right out of in the past two years. It is a very mixed bag.

In most cases, these have been routes where the plan was to fill airplanes at the margins of high load factor major carrier hub markets, and maybe some additional stimulation via cheap fares that the major might not want to match, or even need to match due to strong connecting flows over their hubsite.

The one big downside to this, again, is consumer uncertainty. First, it’s up to the consumer to find and select the new entrant. Next, the media cost of breaking into a large metro is a rap-stopper. Then, in non-leisure markets, low frequency or day-of-week schedules mean the consumer has to shoehorn travel into itineraries that aren’t attractive.

The hard fact today is that both Frontier and Spirit are on the hunt for a viable role in the air transportation system. It remains elusive, and combining the two fleets won’t change that.

The fact is that the traditional ULCC model is essentially gone. The option of spreading operational costs over more and more seat density is now run out. Plus, the march of pattern bargaining in the airline industry is putting the kibosh on any real labor cost advantages this genre once had.

Spirit appears to have a grip on the future. Cutting back flying, and refocus on leisure destinations, instead of trying to shadow-schedule majors in high-density hub markets, clawing for a share of the local O&D. Not sure about where Frontier is headed, notwithstanding a reported profitable 2024 4th quarter.

At this point, it’s hard to get a vision of what market strength will come from just adding another 172 airliners to the Frontier identity.

The key to watch: Frontier will likely come back with other proposals for Spirit. If the deal is rich enough for NK creditors, it will be a done deal. Creditors and lenders won’t be concerned whether the transaction will result a successful airline or not. Their fiduciary responsibility is to cash out, period.

Waiting: The Frontier proposal is vintage uncertainty. How they move ahead to craft a merger plan that eliminates consumer uncertainty will be interesting to see.

Otherwise, the result will mostly be a bonanza for airliner paint shops.

____________

Monday, February 4, 2024

Air Wisconsin: Charting The Disappearance

of The Independent “Regional Airline” Sector

Several weeks ago, American essentially announced their decision that they no longer needed to lease airliners from Air Wisconsin, effective in April.

Regardless of how this event is spun on the Walter Mitty websites, this is not a great situation for Air Wis, which is now laying off over 500 employees. Please, it’s not even vaguely credible to conclude that this was a unilateral decision by ZW – dumping a contract with AA in favor of chasing uncertain and limited EAS contracts.

The lift provided by Air Wisconsin will be replaced by other capacity in the American Airlines fleet. The consumer won’t be affected.

That means that ZW is saddled with a fleet of sixty 50-seat CRJs, all dressed up with nowhere to go. At least until it figures out a future path.

Opportunities? The carrier now is looking at EAS contracts, where the competition is immense and highly cost dependent. The problem is that the there’s a lot of lead time for these contracts and nesting several dozen CRJs on the EAS program means lots and lots of contracts need to be won over a very long period of time.

Charters are an option, but iffy in regard to dependable revenue streams.

One clear fact: operating as an independent brand as it once did is out. That air service need is long since gone. Attempts by entities such as ExpressJet, and Prestige and Independance Air went 86. The role of air transportation in the USA has evolved totally since the days when Air Wisconsin was selling seats, taking reservations, issuing tickets on its own stock, negotiating joint fares, and operating a geographical route system under its own identity.

Also, over these years, the communication needs of America’s business base have changed, materially torpedoing the value of most short-haul, small community O&D demand.

Take a look at, say, 1983. “Regional airlines” were booming in a post-deregulation marketplace, and the potential feed traffic they generated became important to major carriers. That led to simple code-sharing, and later in the decade the full move from just code-sharing between majors and independent regional airlines to outright leasing deals.

This eliminated most of the vestiges of the geographic route systems these small carriers once operated, and the infrastructure attendant to an independent airline operation. The structure today is to lease planes along with their crews, to fly as part of the major airline systems, at the schedule provided by the major customer.

While this was unfolding, another major communication shift took place. Historically, robust O&D markets such as BDL-LGA or ALB-BOS, or ABI-AUS were supported by people carrying communication between such points. In briefcases, mostly. Or the need to do a face-to-face with the planning team. Or whoever needed the information and data that the human was carrying.

Take a look. That information and communication no longer needs a human to board a C99 and deliver it in person to the meeting in Syracuse. That’s being done largely electronically, and the need for an airline passenger as part of the channel is gone. Toss in the comparative and increasing cost of air travel, and we have a situation where much of the original underpinning of small community O&D traffic has simply evaporated.

The point here is that, while there may be some innovative applications for the ZW fleet, it won’t be in resurrecting the air transportation system in which the carrier originated.

The “regional airline” industry, as an independent transportation system supported by now-obsolete communication modalities, evaporated two decades ago.

More changes coming in 2025.

__________________

Monday, January 27, 2024

The International Opportunity For Mid-Size Airports:

It’s A Different Game

Condor’s Trans-Atlantic Program Cancellation: Don’t Misread It

New trans-Atlantic service opportunities are coming into focus.

As far back as 2016, we’ve been making clear that secondary USA airports will be facing strong opportunities for trans-Atlantic markets, with the entry of the A321XLR.

But on a wider note, there have been material changes in the global air service structure that dictate that every USA airport needs to factor in international access to their long-term economic planning. It’s access, and that means more opportunities than whether there are international nonstops at the local airport.

This dynamic is already in progress in the trans-Atlantic sector. And the usual suspects are now confidently “forecasting” this new potential. The problem is that most of them are just assuming the performance capabilities of one or two new airliners will magically make international access a snap.

Wrong.

Lots of “studies” are in progress, expensively and blindly whacking away at a mythical pinata of potential markets to “lure” carriers to fly to town from afar. The concept of geopolitical realities and air service demand realities are completely missed.

Intentionally, in some cases. Ignorantly in others. What’s critical is that airports take the effort to understand the challenges and the opportunities. Traditional ASD metrics and assumptions don’t apply.

The Condor Message. In the last month, Condor chopped Frankfurt flights from four USA airports, including PHX and SAT, and a couple in Canada. For airport planning, this is a very important event, the causes of which must be factored into any airport’s international planning.

Leisure Traffic Isn’t In The Play. One might think that low seat-mile cost A330s would experience strong traffic. But it was focused on leisure travel, with flight frequencies appropriate to that sector. That is not a harbinger of the EU business travel that can be generated from, say, CMH, or GRR or JAX to points across the Pond.

Leisure Traffic Isn’t In The Play. One might think that low seat-mile cost A330s would experience strong traffic. But it was focused on leisure travel, with flight frequencies appropriate to that sector. That is not a harbinger of the EU business travel that can be generated from, say, CMH, or GRR or JAX to points across the Pond.

In any case, Condor’s load factors at SAT and PHX were iffy at best. Metrics from our friends at Airline Data indicate that the Alamo City was filling something like 60.4% of the seats. Phoenix did a bit better, but still below 75%.

In addition, Condor’s traffic was dependent on connecting feed to and from Lufthansa. That got pulled when a court ruled that LH was no longer required to participate.

So we have a situation were Condor went after leisure travel and depended on flow traffic to bolster the local O&D. Poof! Failure. Poof! Nothing even close to the business travel potential for trans-Atlantic markets from secondary USA airports such as those noted above. Do not confuse the two sectors.

If There’s No Hub At The Other End, Mid-Size Airports Need Not Apply. This should be the first foundational criteria for any mid-size airport planning EU access: Places like CMH, GRR, JAX, et al must have connecting flow to more than just the nonstop destination.

That means the potential A321XLR (or other) has to set down at an airport where passengers will connect to many destinations. That means an airline with a connecting hub at the EU end.

This immediately culls down and focuses on the potential airline targets. Could be United to the LH hub at Munich. Or American to the BA hub at Heathrow. Or, for forward thinkers, the SAS hub at CPH. The Dublin connectivity of Aer Lingus. Airliners such as the 321XLR and the 737-10 (if and when it gets certificated) represent the ability to access and create whole new traffic flows.

This means the identification of potential carrier targets is dependent to start with two factors: a connecting hub in the EU and a fleet plan that demonstrates the right mix of airliners.

Asia Access For Mid-Size Airports? Other Than Tokyo and Seoul, It’s A Pipe Dream. Okay, let’s talk Asia, which involves a lot more complexity than the emerging trans-Atlantic opportunities.

Recently a mid-size airport in the Southwest grandly announced that they have had great success in “talks” with airlines about nonstops to Asia. There was the usual babble about the Asian investment in the region, etc. The red flag, however, was that they identified Beijing and Shanghai as strong potential markets that should be studied and pursued. Ignorance of the subject matter is no barrier, apparently.

It’s Not A Mystery. There Are Hard Air Service Realities To Start With. Any consultants posturing as international experts would immediately advise the client that the only two immediate potential Asian access markets are Japan Airlines at Tokyo and Korean at Seoul.

It’s Not A Mystery. There Are Hard Air Service Realities To Start With. Any consultants posturing as international experts would immediately advise the client that the only two immediate potential Asian access markets are Japan Airlines at Tokyo and Korean at Seoul.

That pretty much runs the table. There are no other true large connecting airline hubsites on the PacRim.

Other smaller Asian points like Taipei, Manila, and Hong Kong don’t have the connecting power to fill an airplane to a secondary airport in the Southwest. Messing with “studies” and – heaven forbid – political junket visits to these points are clear pork.

These gimmicks are red flags that indicate the consulting project is little more than blind and expensive exploration. Anyone who has knowledge of China, for example, would know from the gitgo that, even aside from geopolitical barriers, China does not have any airports that are even close to being a connecting hub. Even Beijing Capital traditionally it had about a 14% connecting factor. Now with the opening of the new Daxing airport, that’s now split between the two airports.

International Service Is Not A Blank Sheet: There Are Realities That Need To Be Considered. Point: international air service planning is a futurist endeavor. Traditional air service planning and traditional airline structures aren’t in play, necessarily.

Plan accordingly.

And contact us for some hard forecast expertise to help laser-focus your international planning. Click here, and let’s talk.

________

Monday, January 20, 2o24

The New Regime: Hopefully.

It’s one week until a new regime takes over at the Department of Homeland Security and the Department of Transportation.

It is showtime.

Since November, the din around the new administration has been about the border, about international trade, and government efficiency. Lots of fun stuff about buying Greenland, or tariffs on China, or renaming the Gulf of Mexico.

Okay, the time for fun hype is over.

Not much heard about aviation. That’s of concern, especially in light – the glaring light – of the following:

Airport Security. No, we are not sufficiently safe. There have been multiple incidents of common citizens easily finding their way onto the AOA in attempts to stow away on parked airliners. A terrorist would have a field day.

Naturally, the current head of DOT and the DHS have not been heard from. But what about the people about to take over?

What significant changes are in the works to shift the TSA from being a gigantic pointy objects patrol into a true security organization? What actions are going to be taken on January 20 and after to close security gaps at airports?

This is not a matter of waiting six months.

The FAA Mess. The current DOT Secretary last week declared that Boeing has a long way to go to get its act together after the 737Max fiasco and the clear revelations that it had been for years putting share price above all else.

This is like the Gambino Family accusing the Columbo Family of being in the Mafia.

The truth is that the FAA has been a key player in this scandal. Corrupt. It had oversight of Boeing. It is not clear how much the FAA was involved in the 737 MCAS cover-up. It is clear that under the FAA’s oversight, Boeing was even doing maintenance on airplanes without proper paperwork or inspection. That was the case with the door plug that blew out on the Alaska 737 last year.

Any idea where the new DOT secretary stands on this? The silence has been deafening.

The Air Traffic Control Scandal. Yes, it is a continuing scandal – the continuing shortfall in proper and safe ATC staffing. Do a news search on it. You’ll find story after story going back literally decades where the FAA has declared that they have the situation in hand, and more staffing is on the way.

The key indicator here will be who is nominated by the DOT to be FAA Administrator. The current one – despite kudos from across the industry when appointed – is abandoning the post for political reasons as of January 20.

The imperative is to find a person not to just fill the job, but to completely change the job.

Drone Defense Programs. It’s fun to watch the news videos of Ukrainian forces flying small “suicide” drones literally up the tail pipes of Russian tanks. Or actually chasing down individual combatants.

‘Nuff said. No need to say more. Use your imagination. If this is not a gigantic wake up call for AVSEC, the new Secretary of Homeland Security is as dumb as a post.

Advance Air Mobility – What If The Music Stops? Yessir, the future is in small, battery-powered micro aircraft, bringing new transportation channels to cities and metro areas across the USA. That is the mantra, and it’s not to be questioned.

Suitable and sophisticated investors are falling all over themselves in lauding the wonders of having lots and lots 4-seat buzz birds silently moving people around.

The fact is that the concepts as expressed are pretty exciting, even if not fully supported by hard market analyses. But the DOT and FAA leaders need to be very careful not to fall into the hype. Billions of dollars are involved.

In particular, the raw economics of these battery-powered machines have not been proven. Already, Tecnam and NASA have cancelled their electric airliner prototypes due to clear operational, safety and economic factors.

This has been ignored. Plus, the sheer re-structuring of airport and airside facilities has been glossed over, if not ignored completely. The ATC issues have been ignored.

This means that the FAA needs to lead in this area, instead of being heyboys for a burgeoning industry that needs to address a lot of hard issues before it will be even possible to toss hundreds of these things in the skies.

Yes, this is politically incorrect.

Air Service Planning. The days of trying to recreate the 1980s are over. At a lot of rural and small communities’ air access is no longer economically possible at the local airport.

The DOT needs to take the lead in assuring that economic realities are understood, and that alternative access channels be identified. That doesn’t mean pandering to and misleading whole regions with pablum that air service will return.

Final Point: If there are no substantive and concrete programs announced in these areas within the next 60 days, the fear is that more of the same can be expected.

___________

Monday, January 6, 2024

The 2025 Economic Goal for The USA:

Access From & To The Globe.

The Local Airport Is Only One Part of It.

The Crisis Is Here. Get With It Or Get Left Behind. It’s tough to believe how many communities in the USA are chasing off into the economic planning weeds, focused on trendy goals that will get them nowhere.

You can find it by doing a simple news search. Communities and airports working hard to attract (“lure” is the favored term) something called “air service.”

Sounds great, but it’s too often not much more than latter day Children’s Crusades.

At some communities, there is actually is no definition of what “air service” is, beyond having “flights” at the local airport. Or, it gets focused on goals that sound great to the average citizen, but in reality are not much more than objectives that have no relationship with the realities of the airline system.

It’s no different than chasing after “more roads” without a plan for where they might go.

“New study commissioned to attract airlines.”

“Airlines being courted for Denver flights.”

“Southwest is number one air service goal, according to consumer survey.”

“Talks in progress with several airlines.”

These are the leper’s bell of a community being hornswaggled. None of these have any earthly connection to air service realities, or air service knowledge. Fluff.

The #1 Challenge: Defining The Objective Within Realities. It is unfortunate that many communities are chasing “air service” mostly for the sake of having some form of flying machine at the local airport gate.

Or getting misled into studying “service to Denver” or “flights to Chicago” with no scintilla of understanding that it’s the hubbing airlines that need to be focused on, because in 90% of these cases the local community has bupkus chance of generation sufficient O&D to support a Piper Cub, let alone an E175.

Reality: Without Connecting Feed, Most Community Service Is DOA. The fact is that the local region cannot generate enough local O&D even to a Chicago or Denver to make it work, even if an independent airline might get “lured.” (The possibility of which is right up there with chasing sky hooks.)

What they are missing – and to be very blunt, what some “advisors” are intentionally suborning – is that the goal in the future international economy, whether it’s at a community in rural Montana or a metro-peripheral one in the DFW Metroplex, is global access. Comprehensive channels of global access, that is.

Air service is just one part of this. In the coming decade, regions need to think about the total economic and logistical systems necessary to get access from the globe. The truth is that it will be regional, not local, planning that is required.

Ground logistics are critical also. A clear, comprehensive and realistic plan encompassing all channels of communication is the future. The hard fact is that any local air component needs to be developed consistent with how it will support and enhance the total accessibility of the region.

Leisure Flights Are Great. But They’re Not “Air Access.” Just thinking that a couple of O&D flights a week to Orlando is “air service” is an excursion into the economic planning weeds. Great to have, but totally separate from the need of global accessibility.

Letting the city council be bushwhacked with “studies” to “find more airlines” or “recruit Southwest” will go nowhere unless they are tied to and defined by the economic advantages they will bring.

Regionalization: It’s Coming. Work With It or Get Run Over By It. The parochial historical approach to “air service” is AIMBY – it’s absolutely got to be in my back yard. Or else.

Communities across the USA need to shift from local “air service development” to complete programs of “global access development.” Yes, that’s also regional access development. Just having “air service” isn’t the goal – getting the world and its intellectual and hard goods to the region is the difference between economic expansion and getting left behind.

It’s not a supposition. It is not an assumption. Regionalization of all aspects of logistics is as natural as gravity. Communities that recognize this, and plan realistically in a futurist perspective will have the advantage.

Revolution In Air Service Access Planning Is Coming: Standby. Think about it. Take a look at the many airports and communities that have been pandered to instead of professionally guided to optimize the new realities. Year after year of analyses to “lure” local air service that never will come.

At one time, it was vulnerable widows in Boca who were the targets of confidence schemes. Today, it’s small communities that are ripe targets for local air service programs that will go nowhere.

The alternative is to think regional and collaborate accordingly.

We’ll be diving into this with specifics as we move into the New Year. Standby.

___________

Monday, December 23, 2024

Year 2025:

Reality Sinks Into Competitive Strategies

No More Excuses: It’s All About The Consumer

As was just covered in the latest Touch & Go™ vision letter, the difficulty of Frontier and Spirt in breaking into non-leisure markets is a clear path to the blueprint of what we can expect in 2025.

The message is one that needs to be recognized. The economics and consumer dynamics of the airline business have changed materially. The cost of gaining some form of consumer-loyalty, and the systems necessary is going beyond the financial ability of (former) ULCC carriers to pull it off.

Here’s the hard fact, even if it offends some gadfly consumerists and politicians;

There is very limited market room for any substantial new entry into core air transportation markets.

Let’s say it again: There is little potential for any new major competition in non-leisure markets.And it is NOT due to lack of gates, or terminal space, or slots, or other physical facilities. It is due to the sheer expense of getting any form of consumer-preference that can anchor major percentages of the flying public.

The folks at Frontier and Spirit did not just fall off a pickup truck. They are professional planners. They have discovered that breaking into major airline traffic flows faces enormous amounts of money to get the consumer to shift. So, they are planning accordingly. Frontier is dropping over 40 routes in non-leisure O&D markets and retreating back to adding more Florida flying.

This is not because of the nasty major airline octopus killing off new entrants. It has to do with the sheer and foundational economics of airline operations.

As we noted in the T&G, entities such as Avelo, Breeze, Allegiant and JSX are focused on developing differentiated market flows and differentiated consumer products. The recent experience with Frontier and Spirit presents a clear view of the new realities of USA air transportation. No niche, no dominance of any kind, and that means no consumer loyalty.

This enormous amount of investment needed to be head-to-head competition in comprehensive non-leisure markets is something that most analysts miss. It’s critical to gain market share, and just a low-fare, high-density day-of-week schedule won’t do it. A couple of wider seats mean nothing when up against the sophisticated (and investment-centric) service systems offered by carriers such as United.

The usual suspects in congress and in the mushroom gardens of consumerism contend that it’s these nasty big carriers mercilessly killing off new carriers. Sorry, folks. This has nothing to do with David & Goliath.

In most cases, it’s like trying to take on a battleship with a BB gun.

That big airline invested in that air service battle wagon. Despite all protestations to the contrary, it’s the consumer who makes the decision when a new entrant charges into a mainline O&D market. Having sophisticated consumer contact systems, higher frequencies, better trained customer service delivery, and comprehensive national and global access can smother the allure of cheap-with-add-on fares.

That is not unfair competition. It’s a service issue.

One hint: it’s all about what the customer perceives. That’s another point covered in the T&G. Breaking into major O&D business markets is risky and most usually does not deliver, as Frontier has discovered.

No amount of new gates or airport facilities will change that.

Year 2o25: The new game is on.

_______________

Monday, December 16, 2024

Senator Hawley’s Airline Bill:

Without Efforts To Get Clear Facts,

The Public Cannot Be Served

Touching once again on the December 4 Senate hearings on airline junk fees.

Overall, a Senatorial disgrace.

Now, one senator is proposing legislation based on facts not in evidence across the airline industry. Angry rulemaking is bad rulemaking.

As I covered in the analysis and review of that two-hour hoedown, The important take away of that event was that the public really doesn’t have professional, informed oversight of airline operations and policies.

Truth be known, the airline industry itself, at least most of the players, would not have a problem with solid upfront and informed oversight. But what is most unfortunate is that these hearings were not oversight so much as they were attempts to take the airline industry out behind the woodshed to account for any number of real and imagined service failures.

In this case, for those of you out in TV Land who have spent the time watching the hearing on YouTube or whatever channel, you’ll instantly find that it opened with not the attempt to get oversight information, but with a laundry list of convictions to which the airline industry was intended to confess to.

What was revealed in those hearings was a panel of four senators who decided before the gavel first fell that the airline industry was going to be brought to justice.

No problem with that if the content of the questioning was open instead of being accusative and attacking from the start.

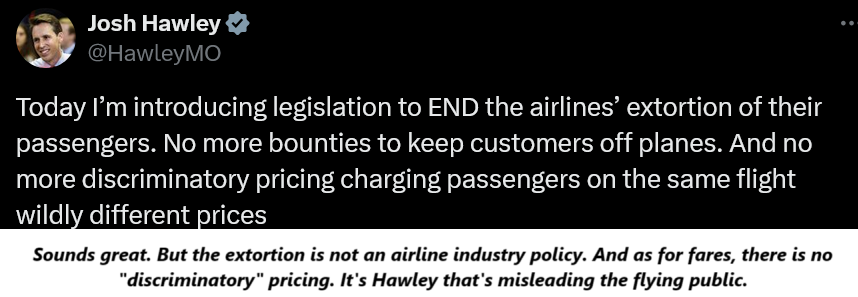

The frustration of these four Congress people has now generated a proposed bill in Congress to throttle airlines. In particular, a bill proposed by Senator Hawley of Missouri that would prohibit all airlines from paying their employees a bounty to collect airline fees. This is just one more indication of how far off the mark the current Senate oversight really is.

Senator Hawley’s intent is positive, but his facts are woefully short. He is implying that all airlines pay their employees a piece of the action when they can catch a recalcitrant evil passenger attempting to skirt airline rules. He has taken a broad brush and is misinforming the public regarding airline policies and procedures. Only one airline is doing this, and it carries a small percentage of air travelers.

Senator Hawley’s intent is positive, but his facts are woefully short. He is implying that all airlines pay their employees a piece of the action when they can catch a recalcitrant evil passenger attempting to skirt airline rules. He has taken a broad brush and is misinforming the public regarding airline policies and procedures. Only one airline is doing this, and it carries a small percentage of air travelers.

(As an aside, Hawley still has anger over an event on American, back in Covid days, where his wife was threatened by a flight attendant of being “blacklisted” unless his 5-year-old wore his mask properly. That was indeed a dark period for air service when cabin crews were tasked with enforcing this stupid rule and did so often very thuggishly. He has a right to be ticked, but that was then, this is now.)

As will be covered probably in the next Touch & Go™ vision letter, we’re going to go over some of the things we see where airlines can shore up their public perception. First up: these are your customers, not petty thieves or vermin gate lice. Second, the customer isn’t always right. But it’s the customer that decides what airline to fly. And today word of mouth is a critical channel of information.

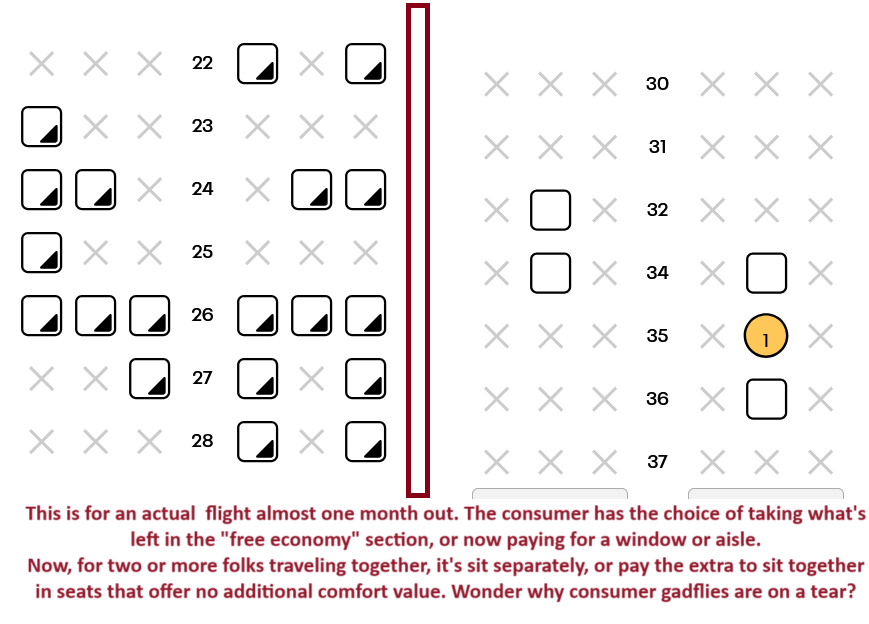

One other little outcome of the December 4 hearing was that at least two airlines had a difficult time clearly explaining what their fee program was and how it was administered. They were unprepared. That led to an enormous amount of anger on the part of the four senators on the panel. It played to the further misconception that airlines withhold quoting fare information until after the booking has been made. Flat not true, but apparently it’s okay in senate hearings.

In the attached deck – which probably most of you have seen – there is a display of a random first page web booking, in this case on Spirit. Completely contrary to the misinformation spouted by a couple of these senators – in particular Senator Hassan of New Hampshire. She literally accused the airlines of first collecting personal data, and then deciding what the fare will be.

Complete dishonest hogwash.

That alone negates any credibility of that December 4 panel. Oversight cannot be done by people who are angry on the warpath and intentionally spout stuff that is untrue. Hawley, pull your bill off the table until you get facts, not angry hyperbole.

The airline industry has a big challenge ahead. This latest hearing is just the start, and the industry needs to manage perceptions of air travel. To be clear, American, Delta and United were ready and prepared, albeit their opening comments were completely ignored by the panel.

That means that for the time being, airlines have angry gate guards, not oversight.

If you haven’t seen our factual review of the December 4 hearing, click here: Senate hearing Dec 4

__________

Monday, December 8, 2024

The Senate Junk Fees Hearing:

It Revealed Another Outrage On Flyers

The media stories – both inside the aviation industry and in mainstream channels – have reported extensively on the December 4 hearings in the Senate regarding airline “junk” fees.

It was based on a report done by the subcommittee:

Senate Permanent Subcommittee on Investigations Releases Majority Staff Report Slamming Sky High Airline Junk Fees

The resulting hearing generated headlines like:

‘Junk Fees’ or ‘Unbundling’? Airlines and Senators Battle Over Added Costs

Airlines make billions charging ‘junk fees,’ congressional report says

Did Anybody Fact-Check The Watch Dogs? The question is whether the folks in the media even bothered do a professional review of what the subcommittee’s report contained, and worse, even bothered to fact check it as well as what was stated at the subsequent hearings on December 4.

We did.

We did.

What was discovered was more that the millions in fees airlines have collected. Something much more damaging to the flying public and the USA consumer.

Anyone who has any clue about the airline industry and has watched and fact-checked the comments made by the subcommittee could not but conclude that these supposed protectors of the public in some cases actually concocted findings that had no connection with reality.

Yes, there are issues with airline service. But that demands oversight that is informed and has complete factual integrity. Certainly, the airlines involved can handle themselves, and are fully cognazant of the political and other sensitivities that must be considered. Overall, the airlines at this hearing were direct, upfront and delivered a stand-up performance.

Regardless of what is going on in airline service, the nation has an additional problem: oversight that is riddled with ineptitude passed off as protecting the public. Blumenthal and his committee have the responsiblity of being fully knowledgeable of the subject matter. It is clear that they failed that metric.

Get ready. Tumble to the fact that just because it comes from a senate subcommittee it is not above the need for fact-checking. Click Here.

Note: The comments and viewpoints herein are specific to BGI. We do not have any client relationship with the airlines involved in this hearing, and has had no contact with these companies or any industry organizations such as A4A.

_______

Monday, December 2, 2024

Airline Seat Junk Fees.

Gee What About Federal Junk Taxes?

One of the things that we hopefully will see ending with the new administration is the use of the airline industry as a convenient political soapbox.