The Effects of The 737 MAX Grounding

Hitting The Three Affected US Airlines A Lot Harder Than Consumers

There’s been some widely-repeated stories implying that the grounding of the Boeing 737 MAX is fixing to dump some real hurt on air travelers this summer.

It’s going to be a nasty summer, according to the reports. Less flights, more demand, and lots of cancelled flights, too.

This is a story angle with lots of staying power.

So, over the next couple weeks, plan for seeing the panting reporters blurting out the dire warnings on the 6PM Ken-And-Barbie evening news show. Reporting live from the local airport – as if that means diddly regarding the subject matter –

“…Airlines will be cancelling thousands of flights this summer due to the MAX grounding, just when record numbers of passengers will be flying…”

Sounds like hard news. But it’s another example of what happens when the media gets hold of data they don’t understand, and still let loose.

Let’s put this in context… which again should remind us that not everything that comes across the TV screen, or on the ‘net is within several zip codes of accurate.

Some hard numbers…

… 6,750 – the number of turbojet-powered airliners in US fleets as of June, 2019, according to the Boyd Group Global Fleet Trend & Demand Forecast.

… 74 – the number of 737 MAX aircraft in US fleets as of the date of grounding… that’s barely more than one percent of the fleet.

… 110 – the estimated number of 737 MAX airliners that would be in US fleets in July, had the grounding not been implemented.

So… do the math… the MAX fleet, even if it were fully in operation today, would represent barely 1.6% of all the airliners operated by US airlines. And that means the “thousands of cancellations” due to the MAX grounding that will supposedly be causing havoc at airports across the country are a drop in the bucket as far as consumers are concerned.

The flights reported to have been deleted from the potential US airline domestic schedule in July and August are under 10,000. Do the math on that as a percentage of the 1,476,000 departures still in the schedule, and that’s a lot decimal points before you get to a number.

That’s no financial comfort for United, American and Southwest, which would have zero problems putting paying passengers into those seats on over 100 additional airliners. They are losing a lot of sure-thing revenue.

A Flight Not Scheduled Is Not A “Cancellation.” But that’s not the same as operationally flummoxing the US air transportation network this summer, which seems to be a headline staple. Remember, too, that only three carrier systems – to be sure, three of the four largest ones – are affected.

Schedule planning at carriers such as Delta, JetBlue, Alaska. Frontier, Spirit, Allegiant, and Sun Country are not affected. So, ATL won’t turn into chaos-city. Neither will MSP or SLC, or DTW or SEA.

As a matter of fact neither will any other major airports, even those where the one of the three MAX-affected airlines have major hub operations… which gets us to the concept of the thousands of “flight cancellations” that are noted in media tomes.

In most of these cases, this is capacity that may have been planned, but was culled out of the schedule. This has already been baked into the inventory and schedules offered by the three affected airlines.

Not to rain on a media frenzy, but passengers are not going to show up at O’Hare next month and find their flight suddenly cancelled at the last minute due to the MAX grounding. Consumers that were early-booked on such planned flights have been mostly re-accommodated, just as is routinely the case when an airline does a schedule change.

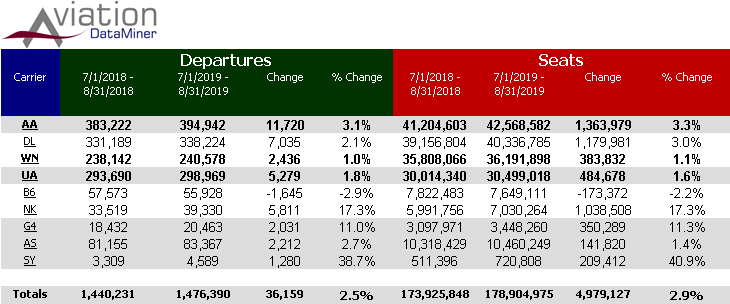

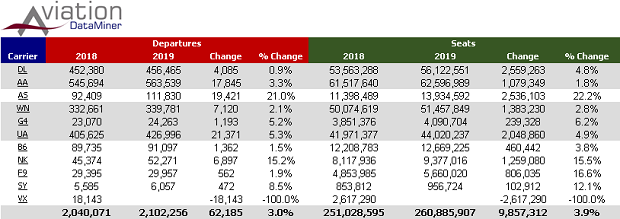

Oh, and the impact of these fewer flights on the total transportation system? Let’s look at the July and August schedules for this year v last year:

We put the three MAX-affected carriers in bold.

Domestically, all three will still be offering more departures and more seats than last year… the industry as a whole will be seeing 2.9% more capacity.

There is no question that with a booming economy, increased spending power, and strong consumer confidence, the three US airlines affected by this grounding are taking a financial hit in lost potential revenue.

But to imply that for the consumer the summer travel season will resemble a re-play of the fall of Saigon is flat inaccurate.

It makes great headlines, though.

________________________________

Monday Insight – May 27, 2019

Due to the US holiday on 27 May, we are again including that week’s update.

Weekly Insight #1…

IAFS To Deliver A “Tour” of China’s Air Transportation System…

In A Little More Than A Year, It’ll Be The World’s Largest

If you haven’t been to China and seen its emerging air transportation system, the International Aviation Forecast Summit will be good alternative.

This year, we’re excited to announce that the Airports:China session of the International Aviation Forecast Summit will be more than just the only independent forecast covering that nation’s top 50 airports.

We are also going to “tour” the many facets of how China is emerging as a factor in global air transportation – and how what is decided in Beijing can affect Bangor, too.

A couple of points that we’ll be covering:

China – The Opposite of Las Vegas. BGI is the only firm that independently researches China-US aviation development. At the IAFS, attendees will get a robust view of how what happens in China, doesn’t stay in China.

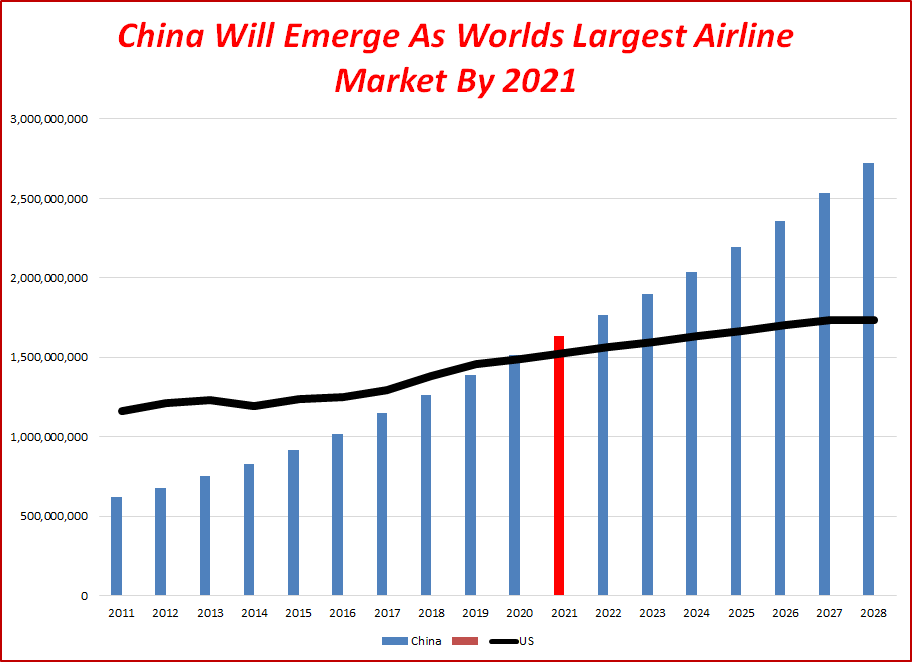

China: The #1 Air Traffic Market. BGI’s forecasts of the top 200 airports in China indicate that the folks at the CAAC in Beijing should break out the bubbly in October of 2020. That’s when China will eclipse the USA as the world’s largest air passenger market.

Lots of China-US Demand – But Mostly For Chinese Carriers. Any material increase in allowed China-US frequencies will mainly enhance Chinese carriers. The growth in China-US traffic will continue, albeit somewhat slower. But the majority of the demand will be carried by Chinese airlines. One reason: China has no true US-style mega-connecting hub operations. That means the majority of service will be from large Chinese cities where US carriers have low/no chance of building brand identity. United Airlines’ experience at Xi’an and Hangzhou are cases in point. But by 2023 the three main Chinese airlines will have connecting hubs at Beijing and at Shanghai, and these will feed their US partners at those airports.

Non-Hubsite US Airports Need Not Worry… China Nonstops Aren’t Coming. The target for nonstops between the US and China will be focused mostly on three categories of destinations in the US: a) major metro areas (NYC, SFO, LAX, ORD, etc.), b) connecting hubsites of US carriers aligned with one of the three major Chinese airlines, and c) several large important leisure destinations.

Other airports, even those in US regions with strong investment from China, won’t be in the play for the foreseeable future.

The reason is that typically, the investment is from all over China, and in the absence of true Chinese airport connecting hub operations, there is insufficient traffic to any one Chinese point. US carriers and their Chinese alliance partners can be expected to focus on expanding service to their US hubs and to major metro areas. But as for developing connective air access to US-China gateways, that’s an imperative for all large US airports.

China’s Airliner Industry – Not Ready For Prime Time. In light of the 737Max issues, there’s been talk that domestic Chinese airliners such as the C919 and the ARJ-21 may be in line for a global order-fest. Actually, while China has moved to the top in a lot of industries, airliners are one they’ve missed entirely. We’ll talk about the reasons China needs the 737. Political posturing aside, they have no other options.

Airports:China is just one of the exciting forecast sessions at the International Aviation Forecast Summit… and they are in addition to the candid views and perspectives from the over 20 airline CEOs and senior executives who will be sharing their perspectives.

If you haven’t registered yet – click here for all the latest, and to get the early registration rate.

________________________________

Weekly Insight #2

Small Community “Air Service Development” Programs

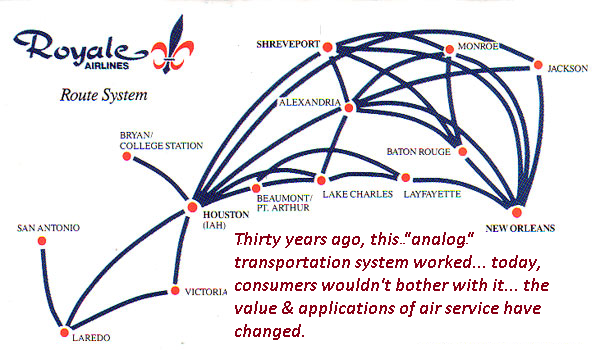

Increasingly, It’s Analog Planning In A Digital World

Last week, another brick-and-mortar chain – Topshop – announced the closing of all its stores in the US and the EU. The high-end fashion retailer’s parent company went into bankruptcy. Over 800 employees got pink slips.

The major reason given was competition with e-commerce retailers. Consumers have found these to better meet their needs.

No point in going into the details, but this is just the latest victim of the Amazon-type trend in commerce. Traditional retailing has increasing difficulty competing with this new channel.

It’s a sea-change in communication, and it’s part of whole new consumer options that are quantum leaps away from what was traditionally available.

Air Service Access Planning: Take Note. And it’s another message for some smaller communities and airports that may be still mired in obsolete “air service development” programs, aimed at bringing back the past.

As we pointed out in last week’s update, all communication channels – including the value and application of the air transportation channel – have materially shifted. Yet most small community air service development programs don’t recognize it.

The New Air Service Consumer Template. We’ll be covering these new dynamics at the 24th Boyd Group International Aviation Forecast Summit this August in Las Vegas, but let’s look at the two market advantages that have established e-commerce. They are pertinent to today’s air access challenges:

… Consumers Want Multiple Product Options… with e-commerce, there’s no wandering around from store to store. A couple of clicks, and the range of options – dozens or more – are displayed and can be immediately determined. That’s a lot different from driving to a shopping mall and wallowing through store after store. It’s also a lot different than having the choice of just two daily flights at the local airport, compared to the dozens that may be available an hour – or even more – away.

… Consumers Want Immediate Results. A couple more clicks, and the desired item can be delivered the very next day in many cases. It’s the same with the higher levels of air access and often more nonstops at that other larger airport down the road. Shoehorning an itinerary into the two flights at the local airport and accessing limited connectivity isn’t consistent with “immediate results” when better options are available.

Lovely Studies… On Yesterday’s Airline System. But take a look – the goals of many of these small-airport ASD programs are the equivalent of trying to re-establish brick-and-mortar channels in an e-commerce world. Often, the service that many small communities can attract to the local airport meets neither of the above criteria.

It’s unfortunate that some small communities have spent hundreds of thousands of dollars on “true market studies” or “leakage/drive” analyses or unscientific consumer surveys, all aimed at getting back traffic that, like at retail stores, has long since left for more effective ways of communicating.

It’s A Consumer Decision – One That Often Can’t Be Changed. The challenge of convincing an airline to toss more $20 million airplanes into the local airport is just the start. The real work is convincing the consumer to come back and utilize what is often an inferior channel at the local airport compared to what’s available elsewhere.

It’s as silly as trying to convince a teenager to dump his iPod and pick up a Victrola instead. Not only does the kid have not a clue as to what such a device is, but it’s a real bear trying to get a set of 45’s into a backpack.

The Foundational Criteria: Consumer Competitiveness. The one basic necessary criteria for small community ASD: a simple question… Can service be established and maintained that is competitive with alternative consumer options? A viable alternative for at least a substantive percentage of the local consumer base?

In many cases, the answer is yes… but in others, the bottom line is not one that is pleasant to hear.

It’s a question that most traditional ASD programs do not address… or try to smokescreen.

Point: a lot of ASD today is DOA because it doesn’t focus on the new communication realities… instead, some of these programs unethically pander to trying to keep civic leaders unaware of such realities, and the need to pursue regional air access alternatives.

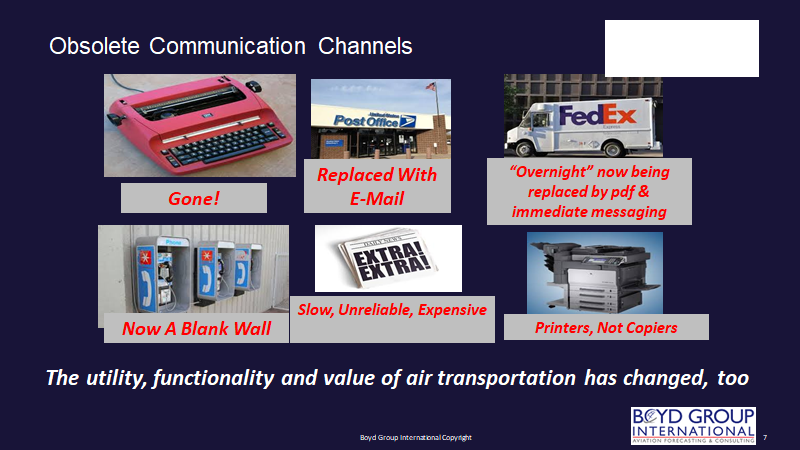

The New Communication Roles of Air Transportation. To start with, increasingly, air transportation is in many applications now inefficient and not time-effective. The emergence of new communication channels – Zoom, Skype, email, etc. – has already rendered intra-regional air service largely dead.

Indeed, flying from Pittsburgh to Hartford/Springfield is a non-starter… as just proven by the demise of such commuter service. And while the blame is put on “lack of pilots,” the real reason is lack of passengers.

As for longer-haul travel, for small and rural airports there’s the pesky fact that an hour’s drive to a larger airport – one with a wide range of “products” and the “quick results” of convenient schedules and nonstop flights – is a consumer factor that no amount of jaw-boning, ARC data, MIDT numbers or other voodoo will change to get these folks to use the local airport’s 2-3 flights.

Access Quality Is The Issue. Today, the #1 transportation and logistics goal of every community must be increasing accessibility with the global economy. This means not just local, but regional approaches, and electronic channels must be accepted as a part of this planning.

Air access is, of course, also a part of this – but in all cases, planning must look at the entire emerging communication picture, not “luring” more flights, without regard for whether or not it is connective.

We’ve often used the example of Muskegon… they have excellent air service. But it’s mostly located down I-96 at Grand Rapids. The two local EAS-supported daily flights – even operated by SkyWest – can barely attract 50% load factors. We could point to Youngstown, or Topeka, too. Consumers have better options than what the local airports can support – and they are using them.

This is not to imply that all air access is out of the picture for many smaller airports. Often, there is the role of being a secondary access point to a region.

But there are consumer realities, communication realities, and complete changes in business and personal interaction channels that a lot of ASD schemes completely ignore by trying to recreate the past.

The Clear New Air Service Template. What has made e-commerce successful is what will determine whether local air service is successful.

It’s a pretty clear template. When there are better options, consumers won’t shop at the local stores – and it’s a functional evolution based on new communication technologies.

It’s the same with the local airport. To ignore these new channels is to ignore the future.

Then, there are BTS data. There are journalists and consultants that download this stuff and purport it to be the final word. There are annual reports from college professors that re-jigger these numbers into not-to-be-questioned tomes that define airline “quality.”

Then, there are BTS data. There are journalists and consultants that download this stuff and purport it to be the final word. There are annual reports from college professors that re-jigger these numbers into not-to-be-questioned tomes that define airline “quality.”

They will be discussing their perspectives of the future at the IAFS™ on August 25-27 at the Wynn/Encore in Las Vegas.

They will be discussing their perspectives of the future at the IAFS™ on August 25-27 at the Wynn/Encore in Las Vegas. Forecaster at A4A.

Forecaster at A4A.

Let’s get real… this is just another clear message that the rah-rah enthusiasm for US-Cuba air service was just a bit pre-mature – like a couple years and a change of government early.

Let’s get real… this is just another clear message that the rah-rah enthusiasm for US-Cuba air service was just a bit pre-mature – like a couple years and a change of government early.

It’s an economic wasteland. Left out of most of the stories about the evil US embargo, Cuba can freely buy goods from anywhere else in the world – just like the US does.

It’s an economic wasteland. Left out of most of the stories about the evil US embargo, Cuba can freely buy goods from anywhere else in the world – just like the US does.