Four Decades of Airline Deregulation

We discuss the disappearance of the independent regional airline industry, and how a lot of small communities are getting hornswaggled by “studies” done by the equivalent of shady used car salesmen… that only keep them from moving into the new communication future…

On December 15, 1978, the government shackles started to be removed from the airline industry.

It was gradual at first, but by five years in, say, 1983, the US airline business was booming.

Let’s take a look…

Nowhere was this more evident than in the regional airline industry … there were over two dozen such small airlines… most were flourishing with their own independent brand identities, route systems and market turf.

Guys In Plaid Jackets Galore. It was boom time for these companies – and for manufacturers of “regional airliners.” At the industry’s annual tribal festivals, a.k.a. conferences of the Regional Airline Association, any attendee with more than a ramper’s title at a “commuter airline” didn’t have to worry about dinner or drinks. Just find one of the phalanx of aircraft sales people and introduce yourself.

This part of the airline business was enjoying huge growth, and so we had the perfect match – airlines looking for deals on new flying machines, and a host of aircraft manufacturers ready to deal – some not too unlike the archetypical plaid-jacketed denizens from rural used car lots.

Invites to fancy meals and lavish “meeting suites” were open to just about anybody with an airline ID. Wine’em, dine’em and sign’em.

There was Beech, Casa, Piper, Fokker, Embraer, Fairchild, BAe, Dornier, Cessna, ATR, Saab, Shorts, deHavilland, all with teams circulating like hungry barracudas to schmooze with the independent “regional” airlines in attendance. The pitch was simple: buy a really great new fleet of Piper T-1040s or Casa 212s and get the jump on your competitor that’s still flying those dumpy old A-model Beech-99s.

And, E-Z financing, too! No cash? No worries! Some of the finance programs were directly from plaid-jacket land.

Lotsa customer targets, too… Fish in a barrel. There was Cascade, Air Oregon, Precision, Rio, Chaparral, Bar Harbor, PBA, Permian, SwiftAir, Southern Jersey, Air Vermont, Atlantis, Down East, Royale, Inland Empire, Air New Orleans, Mesa, Mesaba, Gem State, Aeromech, Big Sky, Golden Gate, Command, Simmons… just for starters… most of them looking for airplane deals.

Again, all of them had their own independent route systems and brand identity. All were expanding and were looking to morph into something bigger. There was no end to the growth of this segment. Small community air service was the future!

Now, while many of these small airlines were well-managed, there were others that were, well, not all that kosher, operationally or financially.

But that didn’t make no nevermind when it came to selling airplanes.

In some cases, the deals included that each new 19-seater would arrive from the factory, replete with a with a check for a quarter or even half million bucks so the airline would have the gelt to get the plane on their certificate – or, maybe, just make the next payroll. It all got blended into the financing.

The future was growth – for not only these “regional” carriers, but for the major carriers, too. No clouds on this horizon.

That Was Just The Start… The Rest Is Less Glitzy. Now, let’s fast forward to today… the deregulation process has continued.

But, unfortunately, most of the airline players so excited about the future in 1983 have not continued. Most of those manufacturers are gone.

So too, with the customers they were pitching back then. But, with the decline in airline players, there’s also a continuing decline in the market for corollary services and support, too. And that process is not played out, yet.

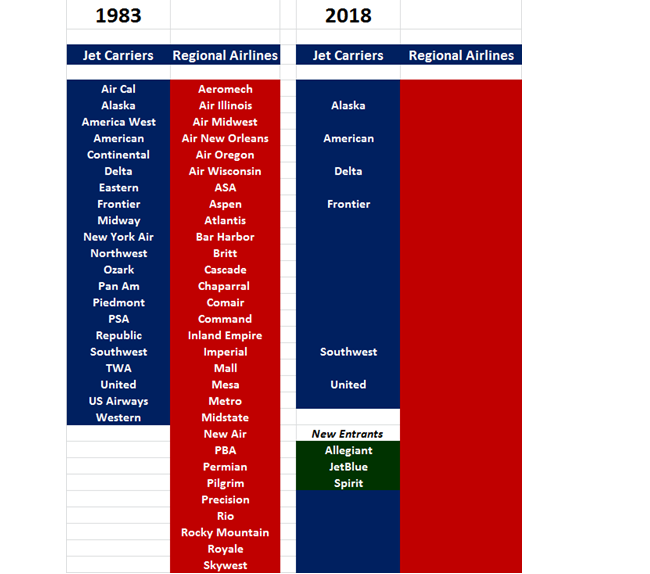

Here’s a quick chart we use to inform communities and airports of the new challenges in “luring” more airlines to town.

The “regional” list from 1983 is not complete, but it gets the point across… not only have those airlines disappeared as independent brands (and most as live companies) but the entire industry that once gathered at RAA conventions is gone too. There is no independent regional airline system, with defined market turf and concrete route systems. It is gone, just like the C-99s, Metro-IIIs, Shorts-330s and the rest of the hundreds of airplanes they once operated.

We could get into the how’s and whys, including some really bone-headed and actually dishonest decisions from the DOT that helped end the existence of independent regionals, but that won’t change the fact that this industry is vapor.

Plus, the major airline sector is also down to just nine major operators… plus Sun Country now entering the ULCC segment.

More Deregulation-Fallout Consolidation Coming In Other Aviation Areas? The decline in airliner players has also consolidated not only the airframe industry, but suppliers across the aviation spectrum.

Related to that, here’s a fact that gets missed way too often when an airport looks to recruit more service…with just these carriers left, there are no airline mysteries, anymore.

Every airline left on this chart has its own strategy, its own fleet mix, its specific route capabilities. Plus, it’s own general turf… the wild expansion seen in the first five years after deregulation is long over. From that, it’s not rocket science to identify which airline systems might have potential to add service (or, conversely, drop service) at a given airport.

Paying To Study The Obvious… That means no giant “true market studies” or “drive capture analyses” or other voodoo translated into giant 80-page documents will change what’s obvious 99% of the time right from the start regarding which airline system might have interest in expanding to a given airport. Airlines have solid market plans… they don’t need some mamaguy consultant studies to tell them their business. (Google it, if you must.)

Or, incredibly, the money still being tossed out at some small communities to simply do studies to find “scheduled flights” – with no first focus on what they may accomplish or whether consumers would use them in light of other travel options, or whether there is actually an airline that could deliver such service – is usually nothing less than buying snake oil. At some point that well is going to go dry.

So it’s amazing – and future-instructive – to see unwary communities get zapped with these expensive rituals, without any prior identification of which of the few airlines left actually can be in the play.

Rural America: A Great Future. As we noted last week (it’s now in the archives), communities of all sizes need to focus on programs to build and enhance global access. That’s a whole lot more than trying to chase the few airlines that are left to fly to airports they can’t profitably serve. It means comprehensive regional planning – involving all modes of communication and logistics. Scheduled flights at the local airport is just one thread – and one that’s no longer economically viable in some cases.

At Boyd Group International, we help our clients focus on future opportunities emerging from the new sets of communication and logistics modalities. Air service is just one of these – and it’s one that has entirely different dynamics than even ten years ago. New approaches consistent with the shifts in the global economy are imperative.

Airline deregulation is just one part of the shift in global communication. There are new opportunities in line.

But in the meantime the plaid jackets are still in evidence – at least for now.

At some point, this myopic pied-piper business is going to consolidate, too. Another victim of deregulation, actually.

A positive one.