Before We Start…

Twenty-two airline industry leaders to present their views of the future at the 24th Boyd Group International Aviation Forecast Summit...

We’re excited to announce that we’ve confirmed Peter Ingram, CEO of Hawaiian Airlines and Maury Gallagher, CEO of Allegiant to join us at the 2019 IAFS™.

They will be discussing their perspectives of the future at the IAFS™ on August 25-27 at the Wynn/Encore in Las Vegas.

They will be discussing their perspectives of the future at the IAFS™ on August 25-27 at the Wynn/Encore in Las Vegas.

Insights Unlimited. Note that we’re in line to hear their views, and their perspectives… other conferences pre-set subject matter “panels” and then shoehorn speakers into focusing on only that issue. At the IAFS™, aviation leaders are free to express their views on the issues that they feel most important.

It’s what sets the IAFS™ ahead of other events… and why the IAFS™ is the most incisive and valuable event of its kind.

Actually, it’s the only event of its kind – an aviation forecast conference. In addition to key airline industry leaders from across the globe, the IAFS™ delivers a range of industry forecasts – from the exclusive Airports:USA® enplanement projections, to aircraft manufacturers’ fleet projections, to a session with John Heimlich, Chief  Forecaster at A4A.

Forecaster at A4A.

International trend and traffic projections, too, including Airports:China™ which will outline what US airports can expect in the next five years in regard to China-US air travel.

Oil prices will drive the cost of jet-A, and that can have material effects on how airlines plan schedules and apply fleet resources. Ben Brockman of OPIS will again be with us to cover what we can expect in the year ahead. We’d point out that his forecasts presented at the IAFS have often been counter to “ambient thinking” – but have been right on the money.

Open Forum – Not Closed Subjects. Our format is one of open discussion and free-form presentations by the leaders in the aviation industry.

At most aviation conferences, it’s not highly informative to sit through boring group sessions, the subjects of which are determined months in advance by conference organizers, and then “moderated” – read, controlled – by somebody with near-zero knowledge of the issue.

Instead, join your colleagues at the IAFS and discover what airline and aviation decision makers see for themselves.

Click here for the latest information and the list of confirmed presenters… and to take advantage of early registration rates.

We look forward to seeing you in Las Vegas!

_____________________________________

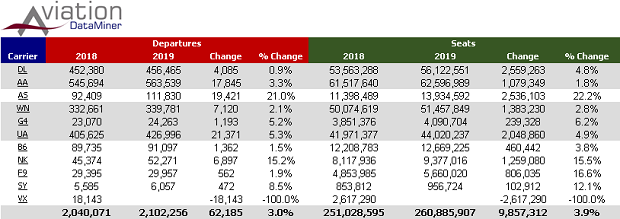

Year 2019 Airport Traffic: Trending With Capacity.

Forecast: Slower Growth

The year-to-date indications are that US air passenger traffic is trending at @3.6% up from 2018.

That’s a lot slower than the full-year 2018 growth of 5.1%, but it does track with airline capacity for the first quarter of the year…

Departure capacity was up at 3.9%, which is in the ballpark with traffic expansion, especially in light of the increasing average aircraft size.

Fundamental Demand v Impulse Travel. What remains to be seen are the on-going effects of traffic stimulation due to ULCC expansion… which tends to create net-new passengers, as opposed to filling air service gaps.

Currently ULCCs represent just over 7% of all seat generation. Based on fleet trends at these carriers, this will edge toward 10% by the 1Q of next year. This will tend to assure that passenger traffic remains above 3.5% for the foreseeable future.

_________________________

And Finally This Week…

Which Came First… The Chicken Or The Egg?

If You’re In Cuba, Neither.

Buttressing the points made in last week’s Monday Update, Cuba has just implemented rationing of things like chicken, eggs, rice, beans and soap.

Yessir, egg production has fallen 25% short of market needs. The Cuban government claims it’s the fault of the US. It’s the only nation in the Western Hemisphere that can claim it’s being attacked by a national omelet shortage.

There’s nothing more subversive than flocks of revisionist chickens intent on bringing down the Revolution.

Let’s get real… this is just another clear message that the rah-rah enthusiasm for US-Cuba air service was just a bit pre-mature – like a couple years and a change of government early.

Let’s get real… this is just another clear message that the rah-rah enthusiasm for US-Cuba air service was just a bit pre-mature – like a couple years and a change of government early.

Beyond the current traffic profiles to Havana, there is no way that large-scale leisure air service can develop to Cuba from the US… it’s not competitive with other destinations.

Load factors to HAV go all over the board month to month, but hover in the mid 70% range on average, and as BGI forecasts indicated, the majority of traffic is from SE Florida.

No clear indication of costs of operation in Cuba, however.

What to watch: In the coming 18 months, the highest and best use of aircraft resources may no longer be tossing 737s to Havana.

_____________________________________